AI Hedge Fund: How it Started

I started investing more than a decade ago.

Back then, my approach was simple and followed a three-step process:

- What are the companies I know and find impressive

- Who are their main competitors

- How do they compare

I would go back and forth between Yahoo Finance and Excel, manually enter the data, and calculate ratios. The quantitative part primarily served to eliminate outliers, particularly companies with high P/E ratios or declining revenues. Then, I would screen the web to uncover information about contracts, partnerships, and what others said about the company.

In January 2016, I prepared a report and shared it with my father for a joint investment. The report took me about a week, and I screened 15 companies. The conclusion of this report was:

- Intel, Google, Blizzard, Activision, Electronic Arts - Buy

- Facebook, Microsoft - Small Buy

- Tesla - Gamble Buy

- SAP, Texas Instruments, Salesforce, IBM, Amazon, Oracle, AMD - Do not buy

- Cisco - unclear

Looking back, the strong concentration in video games makes it clear that I was strongly influenced by my experience at the time.

Over the years, I explored other approaches, such as drawing insights from the options market. I used retail tools like Unusual Whales but failed to gain an edge. On the contrary, this direction led me to attempt “timing the market” using leveraged positions: a recipe for disaster.

For me, the disaster was HubSpot in late 2021, when the company traded around $800 per share in October 2021. Its P/E was above 300 and its price-to-sales ratio in the 30s, as if it were a ‘visionary founder’ story like Tesla, when in reality it was a solid but ordinary B2B SaaS. When I saw the start of a correction and corresponding activity on the option market, I took a short, leveraged position. HubSpot went up, and my account didn’t have enough to cover the margin call when the stock price reached $820. My position was closed forcibly, and the speculative account I had allocated to this strategy was wiped out. The nail in the coffin was seeing HubSpot reach $843, then go downhill to $420 in a bit more than a month.

It is difficult to put into words how angry I was with myself and the situation. I blamed the broker, the market, and, of course, myself for being greedy and arrogant.

It didn’t matter that I was right in spotting an overvalued stock ripe for a correction. What mattered was how much I made. And in this case, I lost my capital, so overall, I was very, very wrong.

Thankfully, the amount at stake was limited and was my own capital. But that was still an expensive lesson I could have avoided. Leverage and short-term timing via CFDs or options are extremely risky if you do not fully understand the instruments and have strict risk limits. It’s tempting, but as Keynes famously said:

The market can remain irrational longer than you can stay solvent

After that, I didn’t make any speculative bets and kept my focus on a more disciplined, safer approach to investing.

To accelerate my research, I decided to double down on automating the stock analysis methodology. That is how I ended up building a first version of undervalued.ai in 2022, to systematically search for undervalued stocks. I used LLMs, first via Hugging Face and then directly with OpenAI. However, the early versions had limited reasoning capabilities, so the pipeline still required me to do a significant part of the research myself.

In parallel, I began managing a family office traditional investment portfolio. This gave me the opportunity to meet and learn from professional fund managers and financial advisors, most of whom were in New York. Overseeing other people’s money is a totally different mindset. You still want to maximise returns but within the scope of your mandate and in a way that is suitable for the beneficiary. So it suddenly becomes optimisation under unbreakable constraints. That said, I had enough leeway, and being skewed towards tech, I increased the portfolio concentration in large tech stocks, with a buffer in treasury notes in case of a correction, to keep gunpowder at hand. A few good entry points, like Meta below 200, Alibaba below 100, and the tech bull run from 2022 to today, made this strategy pay off.

Obviously, there is luck involved. I know investors/fund managers who did way better. But this renewed my confidence and made me focus even more on the financial world.

In February 2025, two things became apparent to me:

- Like most investors, I have persistent biases. I tend to sell winners early and feel losses more strongly than gains, even when the dollar value is the same. Being aware of this is not enough to eliminate it.

- LLMs are capable of handling well-defined analytical tasks in equity research with consistency. Not perfect, but reliable enough if the task is well-defined and the input data is of good quality.

And I started pondering the idea of building an infrastructure that would hand over most of the operational decision-making to AI.

But I had doubts:

- Why not simply invest in indexes and recommend them? Beating the market consistently is incredibly hard, so why not attribute the wins to luck and call it a day?

- Why invest so much time building things myself when I can just use well-established websites or recommendations from much more experienced professionals?

- If it is accessible, why hasn't it already been developed by A-tier engineers/funds/startups? If not, why even bother?

If I had to boil down all my answers, excluding those about self-confidence, to a few sentences, it would be something like:

It is possible. AI capabilities will continue to improve. What matters is consistently outperforming the market, not being better than everyone else.

As a result, I decided to build the AI Hedge Fund : Undervalued.ai.

A first version was rapidly built and released openly in March 2025. Then, the focus was on continuous iteration and improvements. In particular, refining the two core pipelines: the stock analysis and the portfolio management pipeline.

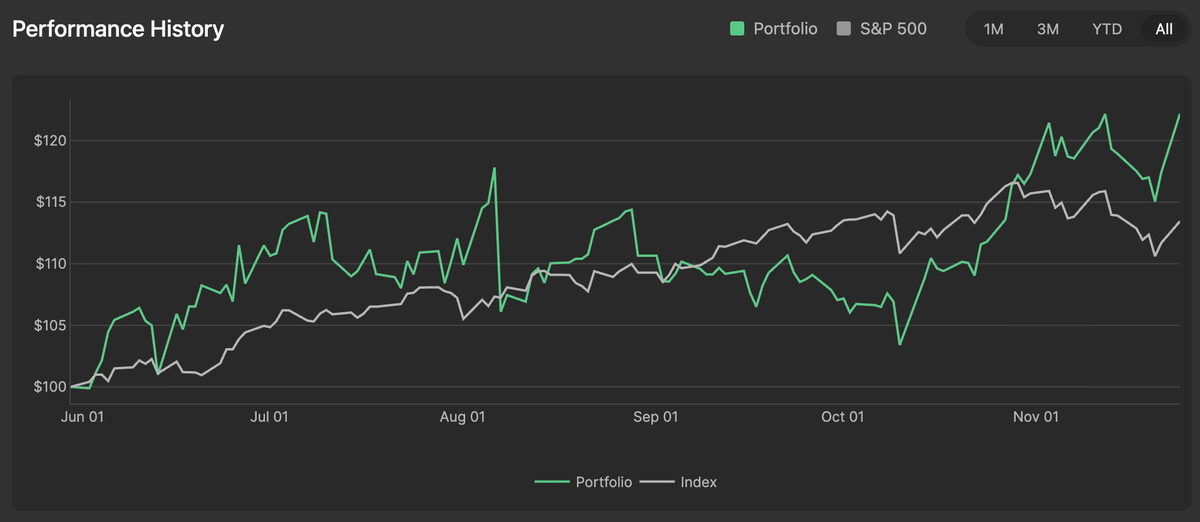

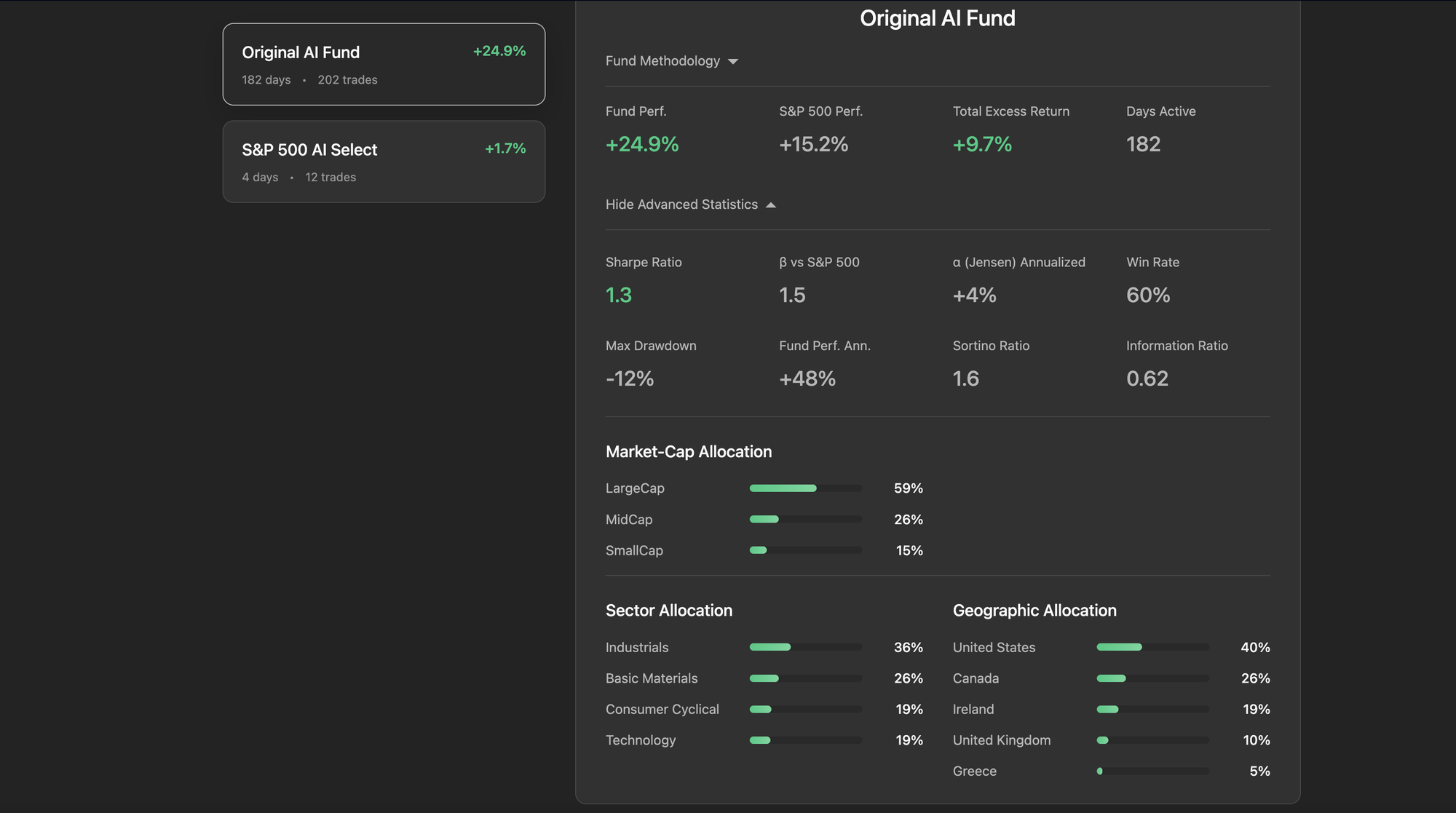

In June, the original fund/strategy was launched and has been running since. By November 2025, and after 182 days and 202 trades, it had the following stats:

- Net Performance*: +24.9% (vs S&P 500 +15.20% over the same period)

- Jensen Alpha: +4%

- And a win rate of 60%

(*)Including fees (calculated from Interactive Brokers). These are live results on real capital, not a backtest. The trade count reflects systematic rebalancing rather than intraday trading.

Those results provide the basis for the next major step: adding the broker to the infrastructure.

I also launched a second strategy: a subset of the S&P 500. In general, the AI Fund infrastructure should allow multiple strategies and is therefore designed with personalisation in mind. For example, the universe and methodology I picked for the Original Fund were pragmatic initial choices based on liquidity (I excluded stocks with low trading volume or market caps below $100M) and other constraints.

The performance of all strategies running in the AI hedge fund is openly and publicly shared on: https://undervalued.ai/funds